Contents

The growing middle class, resilient economic growth, regulatory support and innovation are driving insurance uptake across India. So much so that total premiums in the country are projected to grow by 7.1%, significantly higher than the global average of 2.4%, from 2024 to 2028. At this pace, India will be home to the fastest-growing insurance sector among the G20 countries. One of the most efficient ways for insurance providers to capture this growth is through technology solutions made available by Insurtech.

InsurTech leverages the latest technological innovations to make insurance more affordable, accessible, customer-centric and personalised. This rapidly growing segment is transforming the insurance landscape worldwide, making processes much more streamlined and smoother for both insurance providers and end customers. Insurtech is also gaining popularity in India, reflecting a shift in how insurance products and services are consumed and delivered. S&P Global Market Intelligence report, India boasts the second largest Insurtech market in the APAC region, while Inc42's State of India Fintech Report forecasts that the industry could offer a market opportunity worth $339 billion by 2025.

What’s Driving the Growth of Insurtech?

Insurers are rapidly recognising the power of Insurtech as a differentiator, against a backdrop of changing customer needs and expectations. This is true not just of the Tier 1 cities and metros but also the Tier 2 and 3 towns. The pandemic was possibly the single most important event in changing the Indian mindset towards insurance However, other factors are also contributing to the growth of this sector, such as:

- Technological advancements have increased reach and enhanced conversion rates. Data analytics is further helping insurers identify and target new markets.

- Tailored products are being increasingly offered due to the availability of richer data and better insights into customer needs. Insurtech eases both data analysis and personalisation of products and services while improving underwriting.

- The National Health Stack is expected to drive insurance adoption in India, improving penetration of insurance products, propelled by the evolution of India’s digital infrastructure.

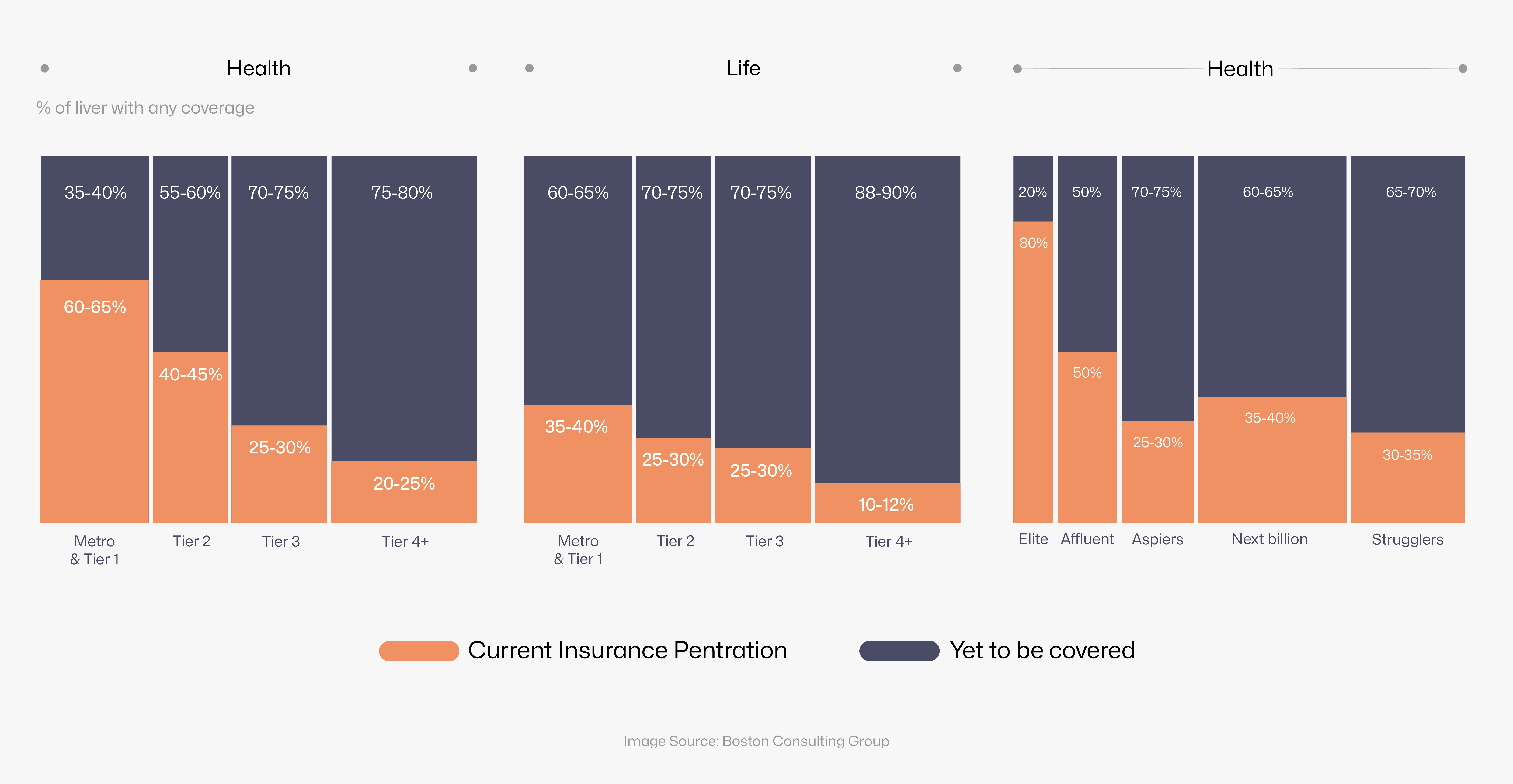

In other words, the potential for increased penetration exists not just across geographies but also across customer segments. The scope for growth in tier 2 and smaller regions is high, as is the potential to penetrate the mid-to-low income segments.

The Role of Insurtech in Transforming the Insurance Sector

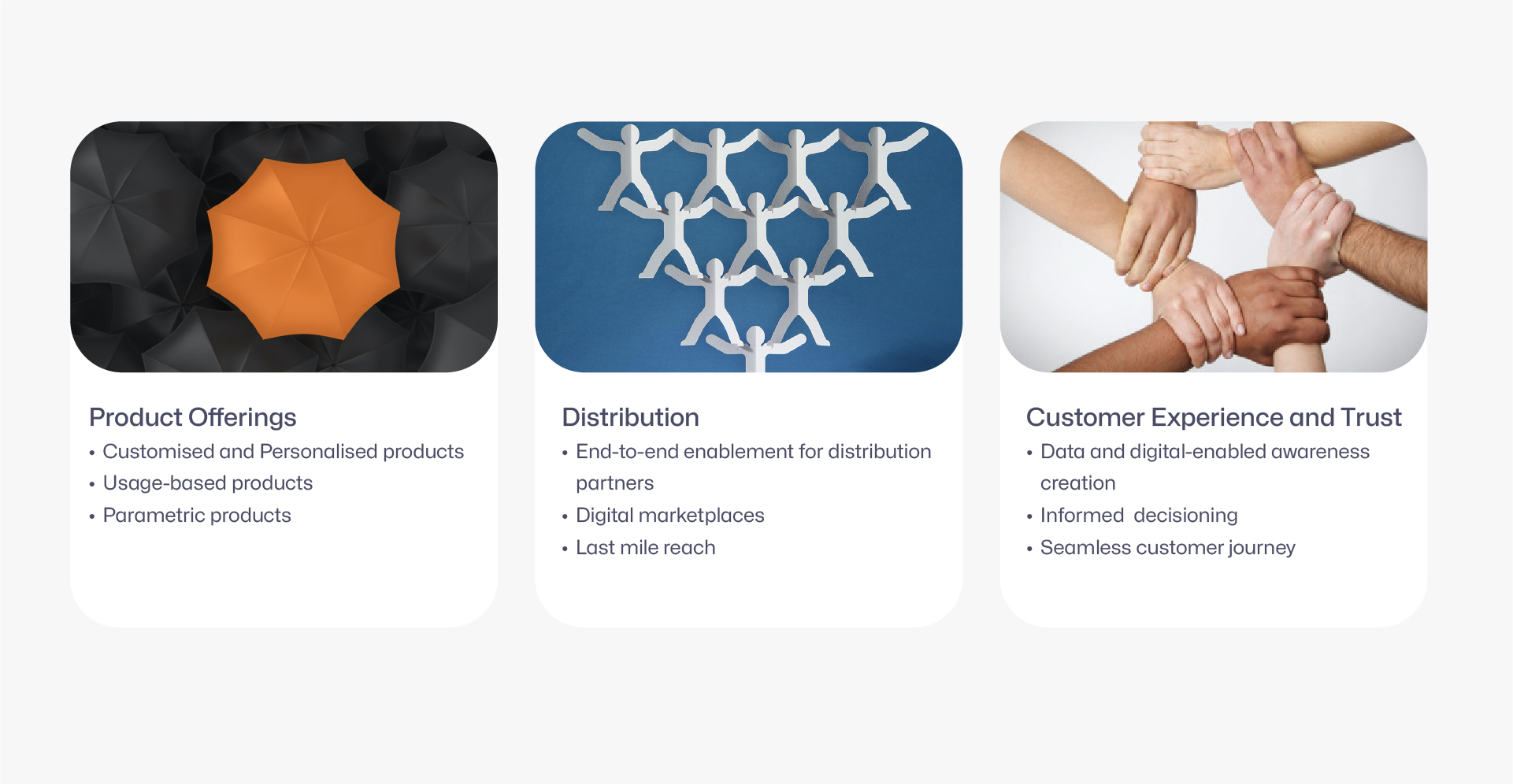

Insurtech offers the insurance industry in India powerful digital tools to increase operational efficiency, shorten time-to-market and meet the rapidly evolving customer expectations. Insurtech companies are constantly innovating to enhance every aspect of insurance.

There are multiple other ways that Insurtech companies in India are supporting the delivery and uptake of insurance across the nation.

Agility in Responding to Customer Needs

Understanding customers’ behaviour patterns, aspirations, needs and expectations has been eased with access to rich data and robust analytics. These insights can be translated into on-demand, just-in-time products. In addition, access to information regarding industry trends and patterns, made available via Insurtech, helps insurance companies in India stay one step ahead of the competition.

Today's customers prefer to interact with brands on digital channels. Technology tools allow insurers to provide self-service facilities, personalised support via AI-powered virtual assistants, and easy access to information for human support staff. Plus, multiple tools for informed decision-making can be offered, such as insurance and premium calculators. Most importantly, technology facilitates the provision of transparent services, which promotes trust among customers.

Faster and More Efficient Claims Processing

The facility to submit claims online has already cut down paperwork and accelerated the claim settlement process. In addition, point-of-impact data, geolocation, application access, etc. are some of the other technologies helping insurance companies gather claim information with minimal human intervention. Providing satisfying customer experiences has also become simpler with the automation of routine tasks that eliminate human errors and delays due to document trail gaps.

Streamlined Underwriting

With the power of AI and data analytics, insurers can speed up and simplify underwriting. With access to customer data, such as credit score, previous claims and even social media activity, risk profiles can be easily created, and appropriate coverage recommended. Insurtech is also allowing insurance providers to capitalise on machine learning tools to automate and accelerate underwriting workflows, improving overall performance and easing compliance.

With the evolution of generative and large language models (LLMs), writing and editing compliant contracts and policies has been eased manifold. Also, tasks such as document review, payment calculation, damage assessment and interacting with customers to resolve issues and provide information can be automated, saving insurers time, manpower and costs.

Improved Risk Management

AI/ML-powered Insurtech tools strengthen risk management by providing access to real-time data and identifying behaviour patterns to effortlessly flag anomalous activity. Digital identity verification is also eased with automated checks on applicants’ information, historical data and CIBIL scores. Early warning signals can be set by establishing key risk indicators (KRIs), allowing insurance providers to take a proactive approach to risk management.

Promoting Disruptive Innovation

Insurtech allows insurance companies in India to take on a more customer-centric approach, which in turn leads to enhanced customer trust and satisfaction. By embracing the latest technology, insurers can offer powerful digital platforms that give customers complete control over their insurance journey, from exploring various coverage options to calculating insurance needs and premiums, receiving instant quotes and accessing 24/7 support. In other words, insurance is becoming increasingly democratised, inclusive and accessible through technology.

Final Thoughts

The insurance industry in India has received a significant fillip from the IRDAI’s commitment to ensure "Insurance for All" by 2047. However, the regulatory body's focus is not just on ensuring access to appropriate insurance policies for all but also on affordable coverage. Insurtech companies will play a key role in facilitating cost-effective policy provision in India. Technology solutions will not only strengthen last-mile reach but also ensure seamless customer journeys through targeted customer communication, product simplification, last-mile activation and cost-savings.

The time now is for all stakeholders, including government bodies, regulators, insurance providers and Insurtech companies to work in collaboration to capture emerging opportunities, drive profitability, ease compliance and contribute to increasing insurance penetration pan-India.

Bibliography:

- https://www.swissre.com/institute/research/topics-and-risk-dialogues/economy-and-insurance-outlook/india-insurance-market-growing-fast-build-resilience.html (last accessed on July 31, 2024)

- https://inc42.com/reports/state-of-indian-fintech-report-q2-2022/ (last accessed on July 31, 2024)

- https://web-assets.bcg.com/c2/b4/466eb6ac4c3c8e5c77aa9ccb921a/india-insurtech-landscape-and-trends-2023.pdf (last accessed on July 31, 2024)

- https://cio.economictimes.indiatimes.com/news/next-gen-technologies/innovation-in-insurance-how-insurtech-is-changing-the-game/101728394 (last accessed on July 31, 2024)

- https://inc42.com/resources/the-insurtech-revolution-indias-leap-from-legacy-systems-to-digital-domination/ (last accessed on July 31, 2024)

- https://www.ibef.org/blogs/digitalizing-insurance-in-india (last accessed on July 31, 2024)

- https://kpmg.com/in/en/blogs/home/posts/2022/11/the-evolving-landscape-of-insurance-tech.html (last accessed on July 31, 2024)

- https://irdai.gov.in/web/guest/document-detail?documentId=1624671 (last accessed on July 31, 2024)