Bangladesh's financial sector is poised for a significant transformation with the imminent arrival of Bancassurance. The Bangladesh market comprises 79 insurance companies, 33 of which operate in life insurance. The banking sector, on the other hand, includes 58 banks.

Low Insurance Penetration Challenge:

Bangladesh boasts a robust banking system but suffers from a meagre insurance penetration rate of around 0.4% (compared to India's 4%) [Swiss Re Institute, 2022]. This translates to a vast, untapped market for insurance products.

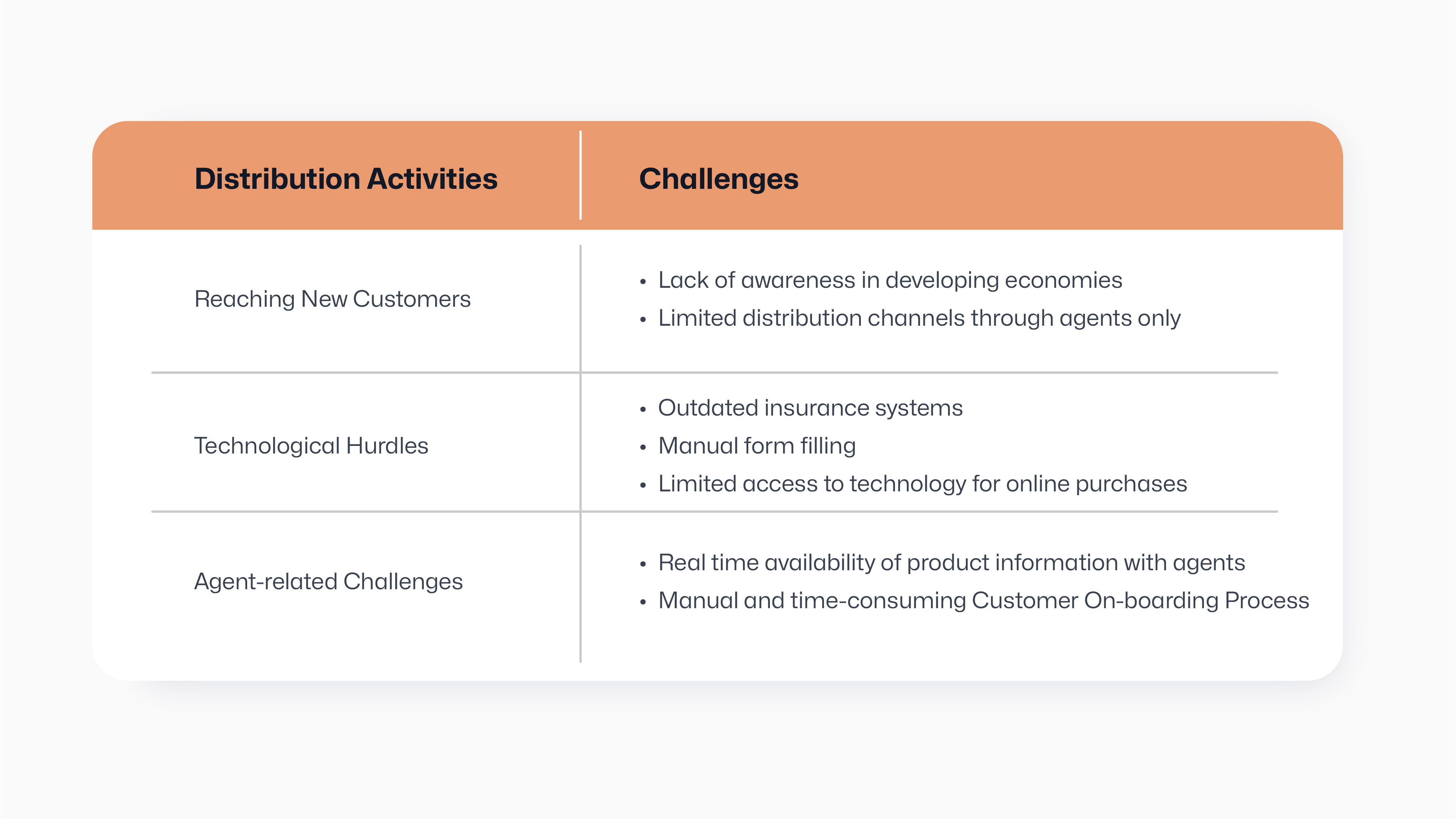

These are a few of the challenges faced by the insurance companies on the distribution side:

These are a few of the challenges faced by the insurance companies on the distribution side:

Barriers for Traditional Insurers:

Barriers for Traditional Insurers:

Distribution Limitations: Traditional sales channels, relying on dedicated agents, are expensive and have limited reach, especially in rural areas.

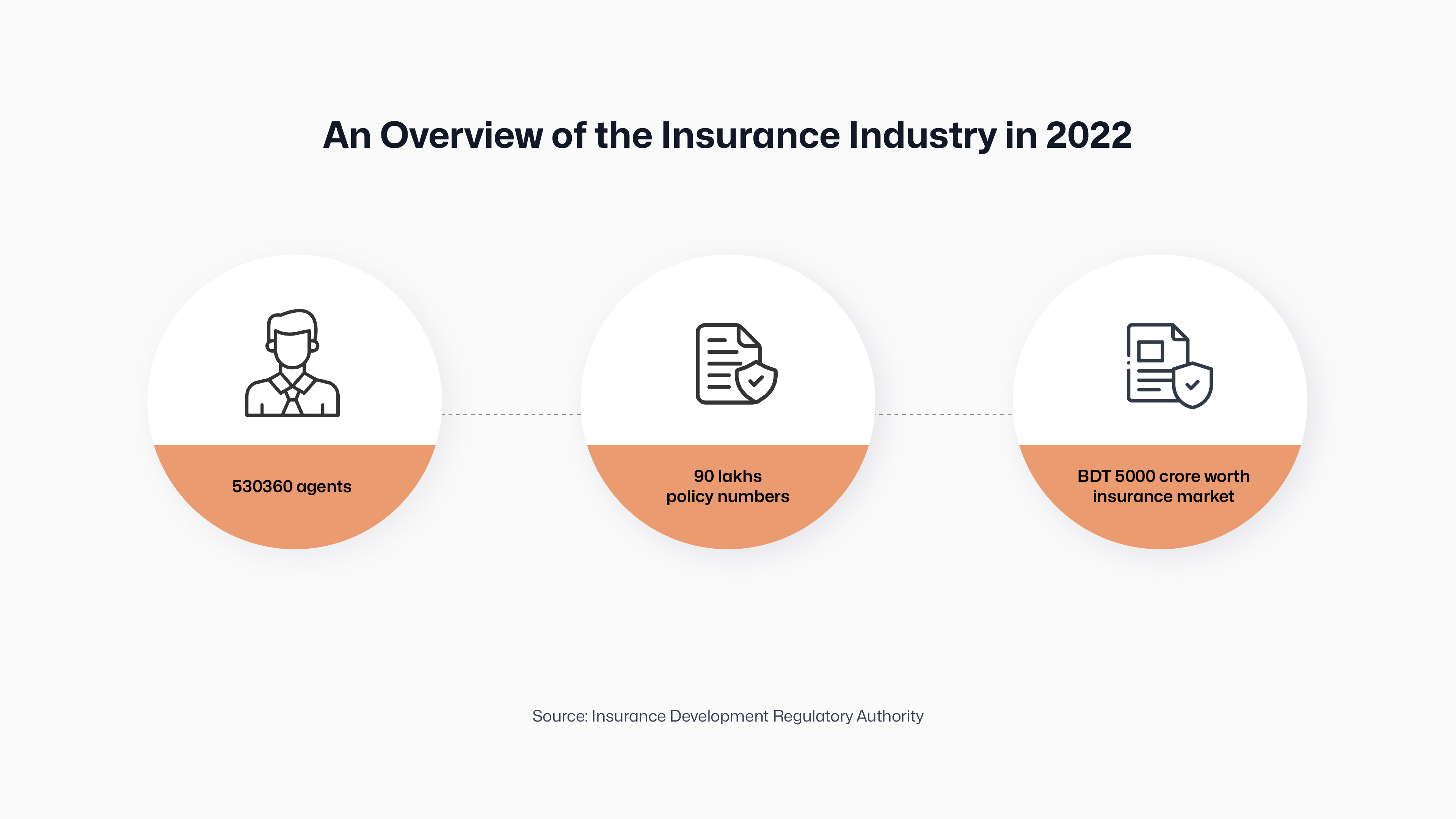

High Agent Numbers, Uncertain Quality: Many agents (530,360 in 2022) raise concerns about training and effectiveness.

Rural Reach Gap: Over 65% of Bangladeshis live in rural areas, potentially underserved by traditional agents.

Issues with claim settlements have dented public confidence in the insurance industry, making customer acquisition difficult.

Bancassurance: A Win-Win Proposition

Bancassurance, an alliance between a bank and an insurance company, makes it easier to sell insurance products to the bank’s customers. Banks hold a distinct advantage in Bancassurance due to their well-established customer relationships. Years of managing savings, and loans, and fostering trust position them as reliable financial advisors. This inherent trust makes customers more amenable to considering insurance products offered by their bank. Moreover, the transparent presentation of these products builds upon the existing bond, creating a seamless path towards a more holistic financial security plan for the customer.

This collaborative setup proves mutually lucrative, with banks generating additional revenue through insurance product sales and insurance companies expanding their customer outreach without the need for additional sales personnel.

For Insurers: Bancassurance offers several benefits for insurers, making it a strategic partnership for reaching new customers and growing their business. Here are some key advantages:

Wider Customer Base and Market Reach: Banks have a vast existing customer base that insurers can tap into. By leveraging the bank's trusted brand and established network of branches, insurers can significantly expand their reach and acquire new customers more efficiently than traditional sales channels.

Cost-Effective Distribution: Bancassurance eliminates the need for insurers to invest heavily in building their own sales force. They can train bank staff to recommend and sell insurance products, reducing distribution costs and increasing profitability.

This can lead to the development of more accessible and need-based insurance products, catering to a wider population and promoting financial inclusion.

For Banks: Banks can enhance their bottom line on insurance sales and enhance their product portfolio, offering a one-stop shop for financial needs.

Bangladesh's digital banking edge offers two key advantages for Bancassurance:

Seamless Integration: Banks' data analysis tools and customer service platforms allow for smooth integration of insurance products within existing banking channels.

Targeted Marketing: Banks' access to a solvent and insurance-ready customer base lets them effectively cross-sell policies through trusted banking relationships.

Bancassurance holds immense potential to revolutionise Bangladesh's insurance landscape.

By implementing a unified interface powered by robust technology and fostering collaboration with InsurTech players, the country can unlock a new era of:

Accessibility: Simplified access to insurance products for a wider population.

Transparency: Clear and convenient management of insurance policies.

Innovation: Development of micro-insurance products tailored to specific needs.

Bangladesh can pave the way for a brighter, more secure future, where increased insurance coverage fosters financial security for all by adopting new technology and enhancing the way of insurance distribution in the country.