Contents

Insurance is being embedded into more customer journeys than ever before — buying a phone, applying for a loan, booking a cab. None of that happens smoothly without APIs. They are the connectors that allow banks, fintechs, and retailers to offer protection products in real time, directly inside their platforms.

The demand is clear: surveys show that 91% of digital bank customers in India would accept an embedded insurance offer if it were convenient, and 63% cite convenience as the main motivator. Globally, embedded insurance is projected to reach USD 802 billion by 2032, growing at 28% CAGR. In India alone, the embedded finance/insurance market is expanding at 46% annually. APIs are the rails that make this growth possible.

Who Uses Insurance APIs Today

- Banks and NBFCs embed credit protection or life cover at the point of loan disbursement.

- Fintechs distribute health or travel cover through apps and wallets.

- Retailers and e-commerce players bundle device protection and extended warranties at checkout, a category that already contributes 43% of embedded insurance revenues worldwide.

- Mobility and logistics platforms attach a trip or shipment cover to rides and deliveries.

These aren’t pilots anymore. APIs are the rails that make large-scale distribution possible.

How Insurance APIs Actually Work

At their simplest, APIs act as the handshake between your system and the insurer’s. A customer applies for a loan, buys a device, or books a ride. Your system calls the API with customer details. The API routes that request to one or more insurers, and in seconds, quotes or policy documents come back.

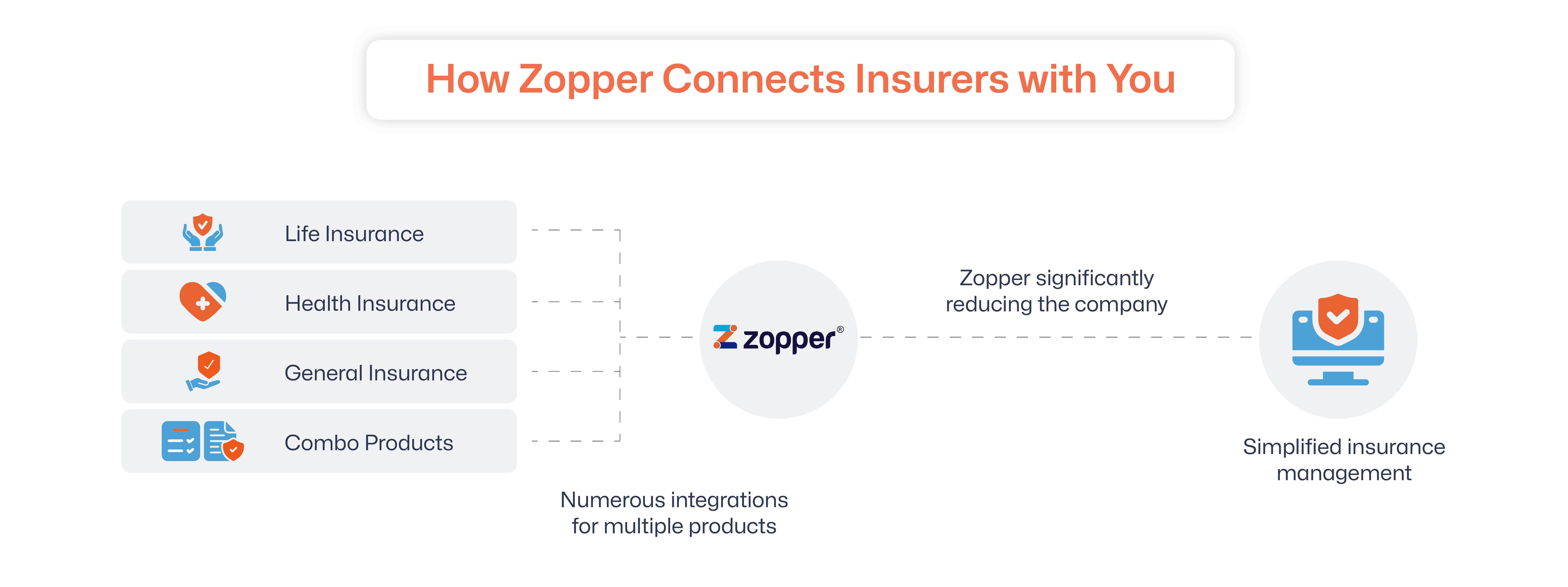

The complexity sits under the surface. Every insurer structures its data differently. Each one has specific compliance checks and rules. Without a connector API, brands have to code for every insurer separately, multiplying the work tenfold. With a unified API, those differences are absorbed behind the scenes. That is exactly what Zopper does: one integration that connects banks, fintechs, and retailers with multiple insurers across life, health, and general categories.

The Main Insurance APIs in an Ecosystem

- Connector or Aggregator API

The connector is the gateway. It links a bank, NBFC, or platform to multiple insurers through a single interface. Instead of building ten integrations, you build one. The API normalises data formats, manages authentication, and handles version updates when insurers change their systems. For business leaders, this means faster launches, lower IT overhead, and the ability to switch or add products without starting from scratch. What it enables:

- A single format across insurers, reducing tech overhead

- Automatic handling of version updates when insurers change their systems

- Flexibility to add insurers or products can be added without starting from scratch

Zopper’s single API plays exactly this role, already connecting insurers and partners at scale.

- Onboarding and KYC API

Before a policy can be issued, the customer's details must be verified. These APIs handle Aadhaar or PAN checks, eKYC flows, and fraud prevention. They ensure compliance with IRDAI rules while keeping the process instant for the customer. These enable:

- Regulatory compliance without manual effort

- Lower drop-offs since KYC happens inside the same flow

- Clean audit trails for insurers and regulators

A borrower can have their KYC cleared and their credit shield activated in a single step.

- Quote and Underwriting API

Pricing and eligibility are the heart of insurance. Quote APIs fetch real-time premiums based on customer inputs, product context, return premiums with disclosures, and confirm whether coverage can be offered.

This matters because insurance has to feel instant to the customer. In e-commerce, device protection needs to be priced and shown at checkout, not after delivery. In lending, credit cover must be attached at the point of disbursement. APIs make that possible by shrinking processes that once took days into seconds.

- Policy Issuance and Management API

Once a customer accepts a quote, the policy needs to be activated and documents generated. Issuance APIs handle this. Management APIs keep the policy updated through renewals, endorsements, or cancellations.

Without APIs, issuance often involved exchanging files between systems, leading to delays and errors. With APIs, policies are created instantly, visible both to the customer and the insurer in real time. For lenders and platforms, this means lower back-office costs and better customer trust.

- Claims API

The ultimate test of insurance is the claim. Claims APIs allow customers to file, track, and settle claims digitally. They connect directly with insurer systems to validate documents, adjudicate claims, and update payout status.

This is where embedded insurance either earns trust or loses it. If a customer who bought coverage through a loan app can file a claim within the same app and track it transparently, adoption will grow. APIs make that seamless loop possible.

- Cross-sell and Attachment API

These APIs power contextual selling. They surface the right insurance product at the right moment like credit protection with a loan, warranty at checkout, travel cover with a booking.

The data shows the impact: electronics and device protection already account for more than 40% of embedded insurance revenue. With APIs, these offers can be timed perfectly, priced dynamically, and issued instantly.

From Fragmentation to Flow

The question “Where are the insurance APIs?” used to have a frustrating answer: scattered across portals, half-manual, and rarely integrated. Today, the answer is clearer. They’re here, they cover the full lifecycle from onboarding to claims, and they’re increasingly available through unified connectors.

For banks, fintechs, and retailers, that means the real decision isn’t whether to use APIs, but how many integrations you want to manage. A single API layer, the kind Zopper provides can turn a fragmented mess into a streamlined ecosystem.

https://www.mordorintelligence.com/industry-reports/embedded-insurance-market