Contents

What is Retail Assurance?

Retail assurance represents a specialised segment of the insurance industry focused on protecting consumer durables at the point of sale. Unlike traditional insurance models, retail assurance integrates seamlessly into the purchasing journey, offering customers immediate coverage for their electronics, appliances, and other high-value items.

Consumer durables insurance encompasses various protection plans, including extended warranties, accidental damage coverage, theft protection, and performance guarantees. These plans bridge the gap between manufacturer warranties and comprehensive insurance policies, providing tailored coverage that addresses the specific risks associated with modern consumer electronics.

The industry serves multiple stakeholders: retailers gain additional revenue streams and enhanced customer relationships, and manufacturers reduce warranty costs and improve brand loyalty. At the same time, consumers receive peace of mind and financial protection for their investments. This ecosystem approach has made retail assurance an integral part of the consumer durables market.

Modern retail assurance goes beyond simple warranty extensions. It includes innovative coverage options, such as subscription-based protection and embedded insurance, that can be activated at the time of purchase.

The Evolution of Consumer Durables Insurance

The retail assurance landscape has shifted from basic repair extensions to a high-tech ecosystem:

- The Early Era (1960s-80s): Protection began as a simple "time extension" on manufacturer warranties for major appliances, primarily serving as a secondary revenue stream for retailers.

- The Digital Shift (2000s): The explosion of smartphones and laptops exposed the limits of traditional warranties. Consumers needed coverage for modern risks like theft, liquid spills, and accidental damage, which manufacturers didn't cover.

- The Modern Standard (2020s-Present): Driven by the pandemic’s dependence on home tech and supply chain costs, assurance is now a digital-first necessity. Today’s model uses AI for risk assessment and APIs for instant, paperless claims, moving from a "reactive fix" to a seamless ownership experience.

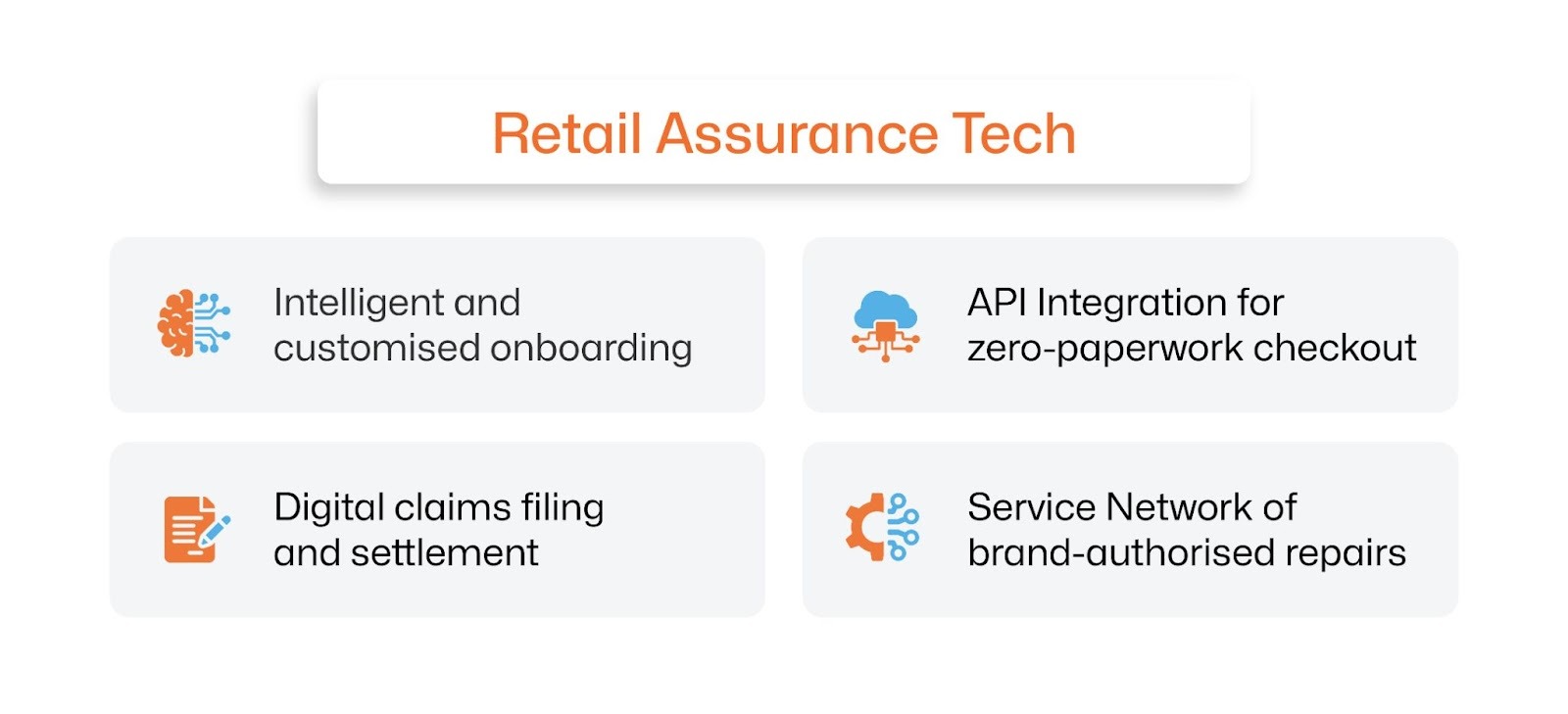

How Retail Assurance Works

Modern retail assurance is a tech-driven orchestration between the retailer, the platform, and the service network.

- Intelligent Onboarding: Sophisticated algorithms analyse product data and historical claims to recommend the best coverage. This ensures customers see relevant options, such as phone screen protection or appliance coverage, while retailers maximise their margins through data-backed pricing.

- Digital Integration: API-first systems sync directly with retail software to capture transaction details instantly. This removes manual paperwork and cuts enrollment time from minutes to seconds, ensuring no delays at checkout.

- Touchless Claims & Policy Management: Technology has simplified the entire ownership journey. Through mobile apps, customers can manage their policies, file claims using image recognition, and track repairs in real-time. Processes that once took weeks are now resolved in hours.

- Unified Service Ecosystem: A strong repair network is the foundation of the program. By integrating brand-authorised service centres and specialised logistics, the system ensures quality repairs with genuine parts. Beyond basic fixes, modern programs offer value-adds like data recovery, loaner devices, and even upgrade options if a repair is not viable.

Business Models in Retail Assurance

The retail assurance industry operates through several distinct business models, each offering unique advantages and addressing different market segments. Understanding these models is essential for retailers, manufacturers, and technology providers seeking to participate in this growing market.

Direct Retail Model

In this model, retailers develop and manage their own protection programs, often partnering with insurance carriers for underwriting and claims processing. This approach offers maximum control over pricing and customer experience, though it demands heavy internal resources for logistics and regulatory compliance. Major electronics retailers like Best Buy have successfully implemented this model through their Geek Squad services.

Third-Party Administrator Model

Many retailers prefer partnering with specialised third-party administrators who manage the entire protection program lifecycle. These partnerships allow retailers to offer sophisticated protection plans without developing internal capabilities. The administrator handles everything from product development and pricing to claims processing and customer service.

Embedded Insurance Model

Extended warranty programs increasingly incorporate embedded insurance principles, with protection automatically included in the purchase price or offered as a seamless add-on at checkout. This model reduces friction in the enrollment process and can significantly improve attachment rates.

Subscription-Based Model

Some providers offer subscription-based protection that covers multiple devices under a single plan. This model appeals to consumers with multiple electronics and provides providers with predictable revenue streams. Monthly or annual subscriptions can include benefits like unlimited repairs, device upgrades, and family coverage.

Each model presents different opportunities and challenges. Retailers must consider factors like customer preferences, operational capabilities, regulatory requirements, and competitive positioning when selecting the most appropriate approach for their market.

Benefits for Stakeholders

Retail protection creates a sustainable ecosystem by addressing specific pain points for all stakeholders involved.

For Consumers

Consumers benefit beyond basic financial protection. Beyond financial safety, modern plans offer peace of mind and practical coverage for real-world mishaps like spills and drops that standard warranties ignore.

Today, protection plans often include benefits like data recovery, temporary device loans, and expedited replacement services that would be costly to obtain independently. For many consumers, these additional services provide more value than the core repair coverage.

Additionally, a device fixed with genuine parts through an official plan retains its value. When it’s time to upgrade, you get a much higher trade-in price because the device has a verified service history.

For Retailers

Selling a device is just the start. Protection plans turn a one-off transaction into a high-margin, long-term relationship.

- Better Margins: Hardware is a race to the bottom on price. Protection plans offer significantly higher profit margins, boosting the overall value of every sale.

- Customer Lifetime Value (LTV): A smooth repair experience builds trust that a discount can't buy. Satisfied customers don't just return; instead, they become brand advocates.

- Reduced Operational Friction: Let the experts handle the headaches. By offloading claims to specialised providers, your floor staff can focus on selling rather than troubleshooting warranty gripes.

- Market Differentiation: In a market full of identical products, your after-sales ecosystem becomes your biggest competitive advantage.

For Brand & OEMs

While retail assurance is primarily driven by retailers and platform providers, brands and manufacturers benefit indirectly through improved post-sale experiences.

- Enhanced Brand Experience: Even if the protection plan is not owned by the manufacturer, a smooth repair or replacement experience reflects positively on the product and brand.

- Customer Retention & Trust: A seamless service journey increases the likelihood of repeat purchases, benefiting the brand in the long term.

- Product Insights: Aggregated claims and repair data can provide valuable insights into real-world product performance, helping improve future designs.

- Reduced Service Pressure (in some cases): Third-party protection programs may handle a portion of post-sale service demand, reducing strain on brand-authorised service channels.

Industry Challenges and Pain Points

Despite its growth and success, the retail assurance industry faces several significant challenges that impact all stakeholders. Addressing these challenges is crucial for continued industry development and customer satisfaction.

Consumer Trust and Perception

Consumer scepticism remains high, often fueled by complex policy language and poor claim experiences. To overcome the perception of "unnecessary add-ons," the industry must pivot toward:

- Radical Transparency: Simplifying terms so customers know exactly what is covered.

- Value Demonstration: Offering benefits beyond basic repairs to justify pricing for those who never face a device failure.

Operational Complexity

Managing a retail assurance program at scale is a logistical balancing act:

- Inventory Strain: Balancing replacement stock across geographies to avoid both capital lock-up and customer delays.

- Service Consistency: Maintaining quality and fair pricing across a diverse network of third-party repair providers.

- Technical Complexity: Modern electronics require specialised diagnostics that aren't available at every service touchpoint.

Technology Integration

Retail warranty management systems must integrate with multiple technology platforms, including point-of-sale (PoS) systems, inventory management systems, customer relationship management (CRM), and claims platforms. These integrations are often complex and require ongoing maintenance as systems evolve. Other concerns include:

- Data Privacy: As plans collect more device and user data, staying compliant with evolving security regulations is an expensive necessity.

- Experience Parity: Delivering a seamless mobile-first journey requires continuous investment in high-quality digital interfaces.

The Scalability Wall

Even the best programs fail when they can’t scale efficiently. The three biggest killers of growth are:

- Friction at the Counter: Slow, manual, and error-prone processes—combined with untrained staff—tank conversion rates.

- Broken Post-Sale Experience: Fragmented claims and disconnected service networks lead to frustrated customers.

- The Visibility Gap: Without a unified view of the entire lifecycle, the business remains unscalable and reactive.

Technology Solutions Transforming the Industry

The industry is moving away from fragmented, manual programs toward a unified digital infrastructure. The focus has shifted from high-level theory to the practical technology that actually drives revenue and customer satisfaction.

1. Intelligent Integration: The End of Manual Error

Reliable assurance begins at the checkout. Using POS-integrated APIs, the system pulls data directly from transactions. This ensures that every policy is issued in real-time with zero "typo risk," creating an airtight audit trail from day one.

2. Digital Enablement: Empowering the Front Line

A program only scales if the sales team feels confident. Modern platforms replace thick manuals with Guided Digital Journeys. Embedded training and automated prompts help staff suggest the right protection plan for the specific device being scanned, removing the guesswork and increasing conversion rates.

3. Orchestrated Claims: A Seamless Post-Sale Experience

The "moment of truth" for any customer is the claim. Advanced End-to-End Workflows replace disconnected phone calls with a single digital flow. From the first notification of loss to the final repair, every stakeholder - the customer, the retailer, and the service centre - sees the same real-time status.

4. Unified Cloud Infrastructure: Visibility at Scale

Scaling across thousands of locations requires a Cloud-Native Architecture. A centralised dashboard provides a single version of truth, allowing you to track attachment rates, claim frequencies, and store performance across your entire network from a single screen. This infrastructure ensures the system remains fast and compliant, no matter how large the volume grows.

Future Trends in Retail Assurance

The retail assurance industry continues evolving rapidly, driven by technological innovation, changing consumer expectations, and new business models. Understanding emerging trends helps industry participants prepare for future opportunities and challenges.

Embedded Insurance

The future of retail assurance increasingly involves embedded insurance that integrates seamlessly into the purchase experience. Rather than selling protection as a separate add-on, retailers will incorporate protection into product pricing or offer it as an automatic benefit of purchase.

Invisible insurance takes this concept further by protecting without explicit customer enrollment. Advanced risk assessment and automated coverage activation can provide protection based on purchase patterns, customer profiles, and product characteristics.

Sustainability and Circular Economy

Environmental consciousness is driving demand for sustainable protection options that emphasise repair over replacement. Future protection plans will likely include carbon footprint considerations, sustainable repair practices, and end-of-life recycling services.

Circular economy principles encourage device refurbishment, component reuse, and material recovery. Protection plans can support these goals by incentivising repair over replacement and facilitating device trade-in programs.

Personalisation and Dynamic Pricing

Advanced analytics and AI will enable increasingly personalised protection plans tailored to individual customer needs and usage patterns. Dynamic pricing models will adjust premiums based on real-time risk assessment and customer behaviour.

Behavioural economics insights will inform the design of protection plans and marketing strategies. Understanding how customers make decisions about protection can improve product design and increase attachment rates.

Ecosystem Integration

Future retail assurance will integrate more deeply with broader technology ecosystems, including smart homes, connected cars, and wearable devices. Cross-device protection plans will cover entire technology ecosystems rather than individual products.

Platform-based approaches will enable customers to manage all their protection needs through unified interfaces that span multiple device categories and service providers.

Conclusion

The retail assurance industry represents a dynamic and growing segment of the broader insurance market. As consumer durables become more sophisticated and expensive, the need for comprehensive protection continues to expand. Success in this industry requires understanding complex stakeholder relationships, embracing technological innovation, and maintaining focus on customer value creation.

Through continued evolution and adaptation, retail assurance will remain an essential component of the consumer durables ecosystem, providing value to consumers, retailers, and manufacturers while driving innovation in protection and service delivery.

Frequently Asked Questions

What is the difference between retail assurance and traditional insurance?

Retail assurance focuses specifically on consumer durables, such as electronics and appliances, and integrates insurance into the retail purchase experience. Traditional insurance typically covers broader risks and operates independently of retail transactions.

How do retailers benefit from offering protection plans?

Retailers gain additional revenue streams with higher profit margins than hardware sales. Protection plans also improve customer loyalty, reduce warranty-related customer service burden, and provide competitive differentiation. Many retailers find protection plans essential for maintaining profitability in competitive electronics markets.

Are protection plans worth the cost for consumers?

The value depends on individual circumstances, including device usage patterns, risk tolerance, and financial situation. Protection plans provide peace of mind and can be cost-effective for expensive devices or customers prone to accidents. Additional services, such as data recovery and temporary device loans, often provide value beyond basic repair coverage.

How has technology changed retail assurance?

Technology has transformed every aspect of retail assurance from risk assessment and pricing to claims processing and customer service. AI enables personalised pricing and automated claims processing, while mobile apps provide convenient customer interfaces. IoT connectivity enables usage-based pricing and proactive maintenance.

What do consumers look for in a protection plan?

Consumers should evaluate the scope of coverage, claim procedures, service network quality, and additional benefits beyond basic repair coverage. Understanding exclusions, deductibles, and claim limits is crucial. Reading customer reviews and checking provider reputation can help assess service quality.

Tags- Retail Assurance, Embedded Insurance, Unified Digital Infrastructure, Consumer Durables